Sustainability & ESG

ISSA 5000 for SMEs: What to Know

Clear overview of ISSA 5000 for SMEs: requirements, assurance options, estimated costs and steps to prepare audit-ready sustainability reports by Dec 2026.

12 February 2026 13 min read

Insights

Practical explainers on ESG, carbon accounting, and sustainability reporting.

Clear overview of ISSA 5000 for SMEs: requirements, assurance options, estimated costs and steps to prepare audit-ready sustainability reports by Dec 2026.

Early planning, verified GHG data, scenario analysis and strong governance are essential to complete the CDP Climate Change Questionnaire and improve scores.

ISO 14064 defines data principles, boundaries, activity data and verification steps to build audit-ready, transparent GHG inventories.

Double materiality turns compliance into strategic insight — 5 steps to map value chains, prioritise topics, validate stakeholders and create audit-ready reports.

Step-by-step guide to implement IFRS S1 and S2: assess applicability, run a gap analysis, set governance, measure GHG (Scopes 1–3) and use automation for audit-ready reporting.

Supplier emissions data gaps undermine accurate Scope 3 reporting — use spend-based estimates, supplier engagement and automation to achieve audit-ready results.

Compare internal engagement metrics with external workforce sustainability reporting, their audiences, key data differences and how integrating both aids compliance and retention.

Explore how LCA scenario analysis modelling Scope 1-3 emissions ensures ISO 14064/SECR compliance and audit-ready carbon reporting.

How AI automates Scope 3 emissions from financial data, improving accuracy, audit readiness and real‑time hotspot detection for firms.

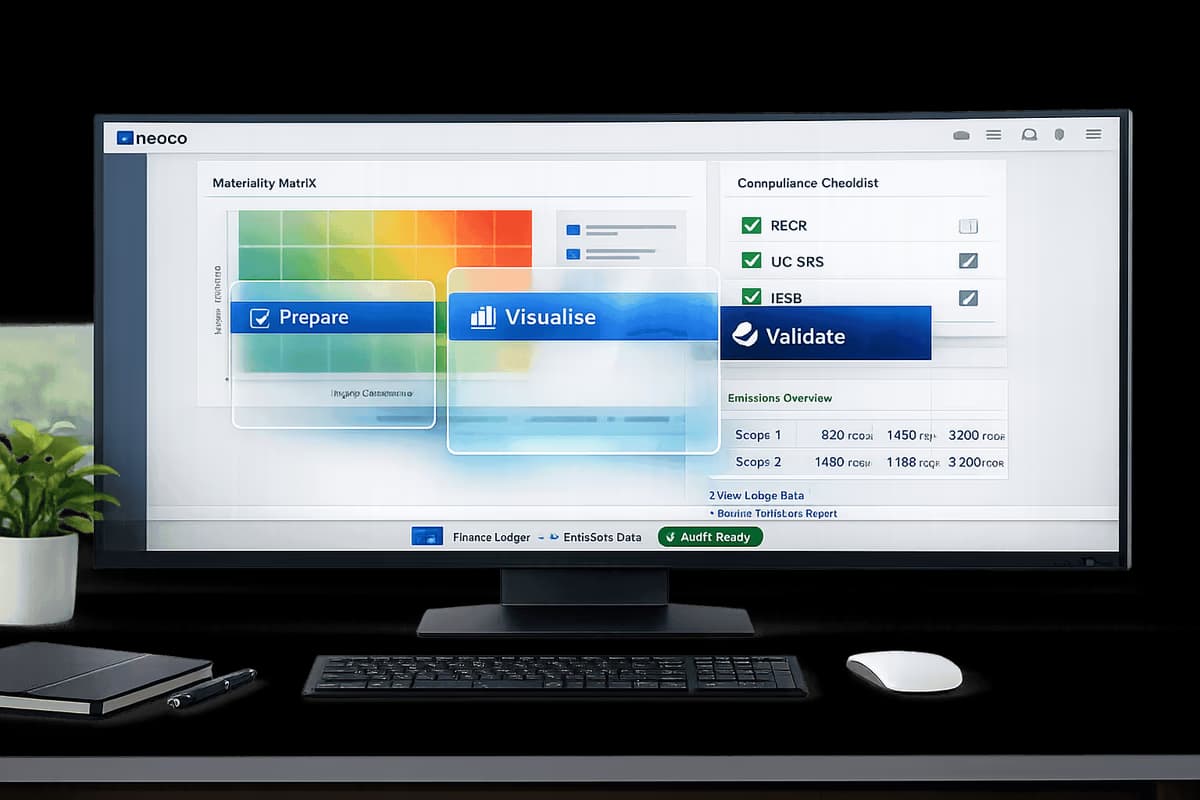

Step-by-step checklist to prepare, visualise and validate materiality data for SECR, UK SRS and ISSB compliance with templates, automation and audit-ready dashboards.

Compare activity-based and spend-based tools for Scope 3 emissions—use spend-based ledger screening for speed, then apply activity data for high-impact accuracy.

Covers UK SRS requirements from 2026 for large organisations, the single‑materiality focus, and how integrated tools map financial ledgers to Scope 1–3 emissions.